eClosings Arrive

North Carolina now allows fully-electronic, paperless real estate closings.

When

my son was in grade school and received letters in cursive writing from

my mother, he asked me to read them to him because he could not.

Schools no longer teach cursive, or only teach it in a very limited

way. To this day, my son has a hard time signing his name to

documents such as his application to Boy Scouts. It turns out this

all may not matter.

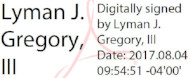

On May 5, 2017, North State Bank conducted the first fully-electronic

mortgage closing in North Carolina. The event, which took a full

year to plan, was so momentous that the North Carolina Secretary of

State and North State Bank’s president attended to witness the event,

and a representative of Investors Title Insurance Company, which

provided the title insurance, monitored the closing. The borrowers

and the eNotary were present at a bank branch in Hickory while the

closing attorney participated by video teleconference from his office in

Charlotte. The borrowers signed everything through a digital pad,

and the eNotary attached a digital representation of the notary seal

and signature.1

Here is a summary of the legal underpinnings that allowed this to happen.

On August 2, 2000, the North Carolina General Assembly adopted the Uniform Electronic Transactions Act.

Among many provisions, this Act allows the use of an electronic

signature, which is “an electronic sound, symbol, or process attached

to, or logically associated with, a record and executed or adopted by a

person with the intent to sign the record.” The definition is very

broad and allows a lot of flexibility in adopting and using electronic

signatures.

The Act, however, specifically disallows

electronic signatures in a number of situations such as the signing of

wills and trusts, notices to cancel utility services, notices of default

preceding foreclosures or evictions, and documents accompanying the

transportation or handling of hazardous, toxic, or dangerous materials.2 Electronic signatures can only be used if all parties to the transaction consent to their use.

Besides the need for electronic signatures,

there must be a way to notarize documents electronically. On

September 13, 2005, the North Carolina General Assembly adopted the Electronic Notary Public Act.

An eNotary must be a licensed North Carolina notary, take an additional

three-hour training class, and register his or her certification to

perform electronic notarial acts with the North Carolina Secretary of

State. An eNotary is empowered to affix to an electronic document

an electronic signature and seal containing all of the information on a

regular notarial seal when the Secretary of State has approved the

eNotary’s electronic information. Significantly, the person

signing must still be in the presence of the eNotary; there is no way

for the eNotary to participate in a signing through teleconferencing.

In addition to authorizing electronic signatures, the Uniform Electronic Transactions Act

also allows for transactions to occur using solely “electronic

records,” meaning a record not on paper. This is the final piece

of the puzzle to allow for a total electronic transaction. There

are, however, some limitations. For consumer transactions that

require information to be provided in writing under applicable laws ‒

home mortgages, for example ‒ the information can be provided

electronically only if, among many requirements, the consumer has

affirmatively consented to an electronic transaction; and the consumer

has received a notice of his or her right to receive records on paper,

to withdraw consent, and to receive records in paper form. In

addition, the consumer must be notified of the hardware and software

requirements for access to, and retention of, the electronic

records. Finally, if a transaction is occurring solely by

electronic means, such as digitally signing on a website only, when the

law requires information to be provided in writing, the consumer still

must receive the documents in paper form.

As you can see, this is an evolving area of

commerce and law. There will still be a slow process of development

until we are more fully completing transactions with no paper, but we

are moving that direction. At Marshall, Roth & Gregory, P.C.,

we subscribe to an electronic signature service provider, and find that

our clients enjoy its ease of use. In addition, we will have an

eNotary available by October 2017. So . . . in conclusion, I am

sincerely yours,

1 For more information about the first all electronic closing, see the May 2017 issue of the Investors Title newsletter NC Connection.

2 This list is not comprehensive.

Other Recent Articles

|

|

|